The insurance industry is notoriously complex, steeped in jargon and tradition. Underwriters have a unique ability to sift through vast amounts of medical and financial data, pinpointing health and life risks within a maze of lab results and handwritten medical notes.

Despite these capabilities, the industry is becoming overwhelmed. With full digitalization, underwriters often receive thousands of pages of repetitive information, and advances in AI have made it easier than ever to generate synthetic data for fraudulent claims. Friendly was created to provide much-needed support.

Upon joining Friendly, I discovered that the San Francisco startup had already invested years in developing AI technology capable of swiftly analyzing extensive medical and financial data. This technology was designed to generate concise summaries, aiding underwriters in making quicker decisions.

The issue was that while we had the technology, we lacked a product. I joined as Head of Product and Design, also serving as a Principal Designer in a player-coach role, to develop a one-year plan to transform our impressive tech into a market-leading product for Automated Insurance Underwriting and Claim Management.

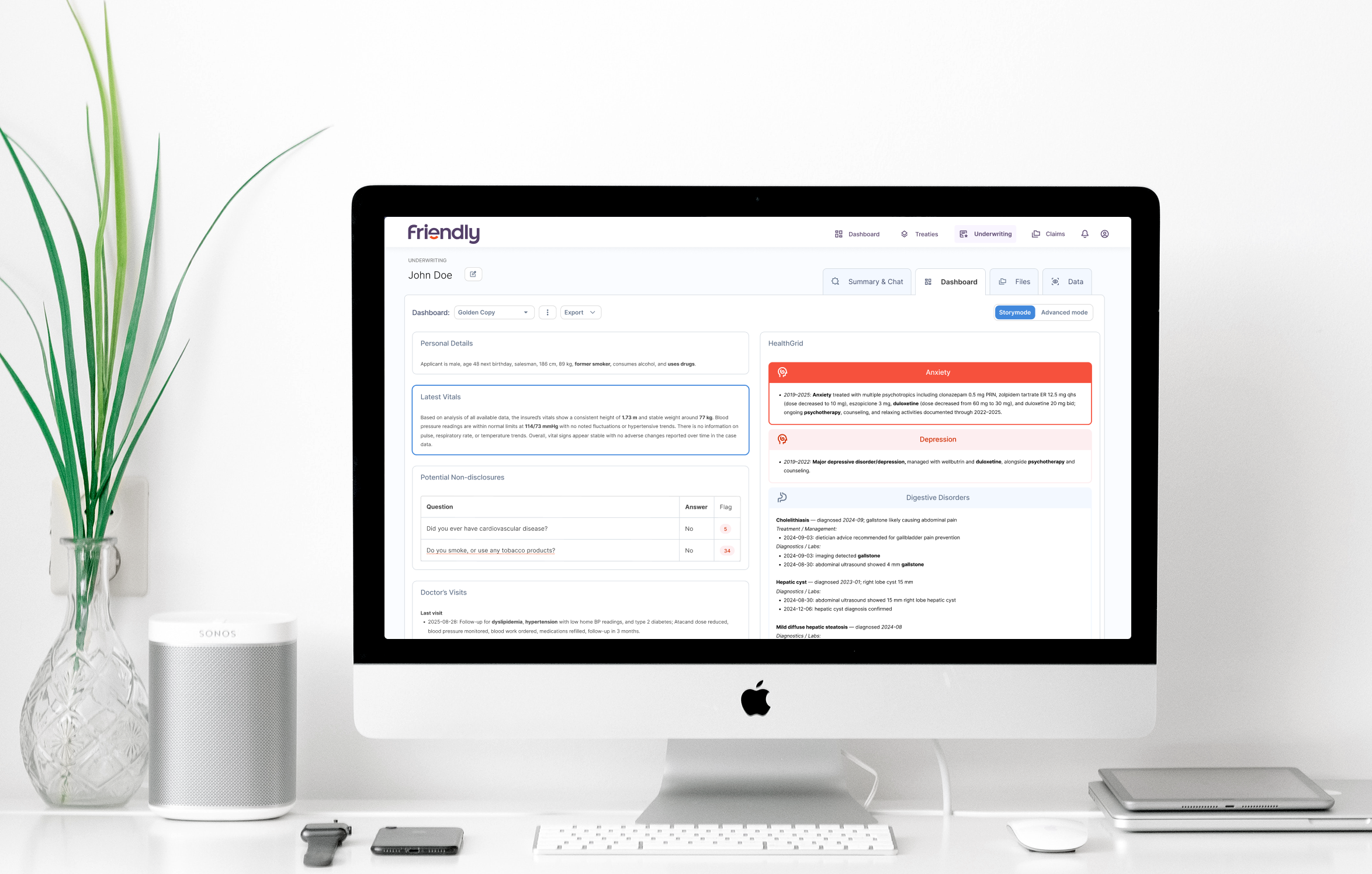

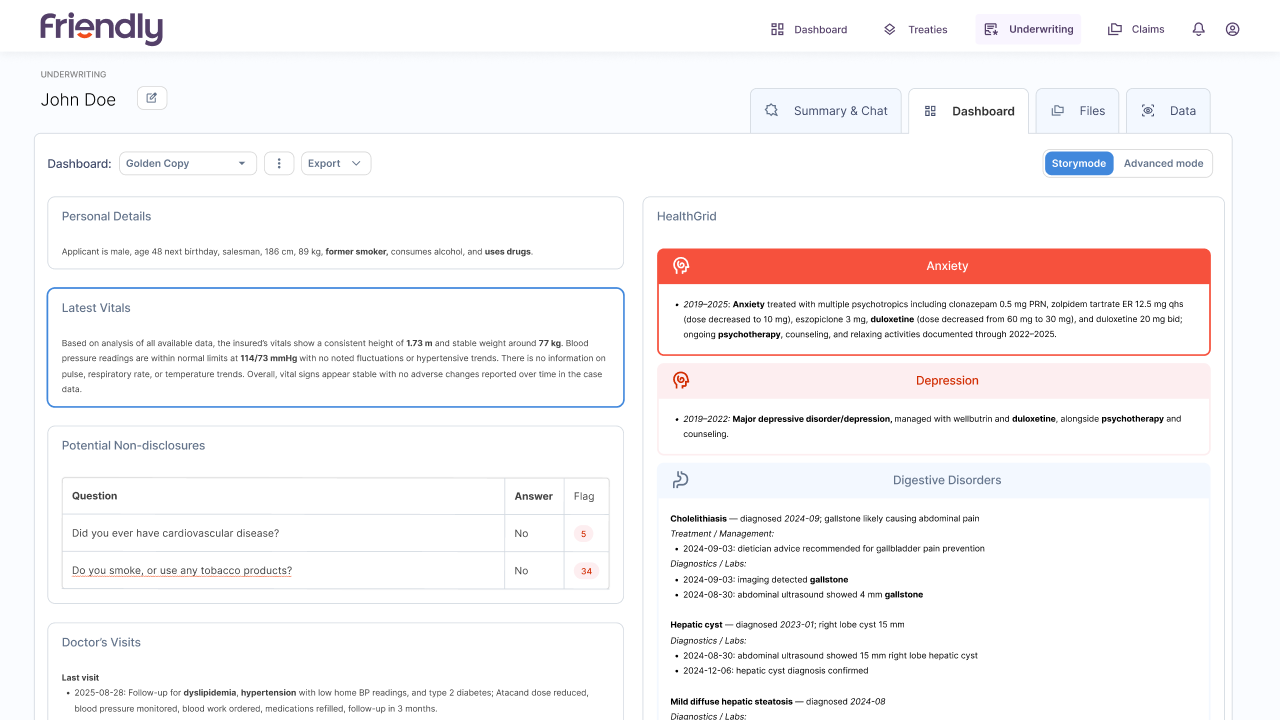

The original user interface featured basic side-by-side panels displaying the source document alongside the AI's extraction and tagging of content.

By the end of the project, we had developed a fully customizable, interactive dashboard equipped with advanced AI features to streamline data organization and facilitate underwriting in minutes rather than hours.

Recognizing that Rome wasn't built in a day, I structured product development into high-impact, cross-functional initiatives. These involved collaboration among Design, Engineering, and Data teams to launch powerful new features every 1-2 sprints. Here's the FigJam of our initiative board:

And some examples of the initiatives that I designed and implemented:

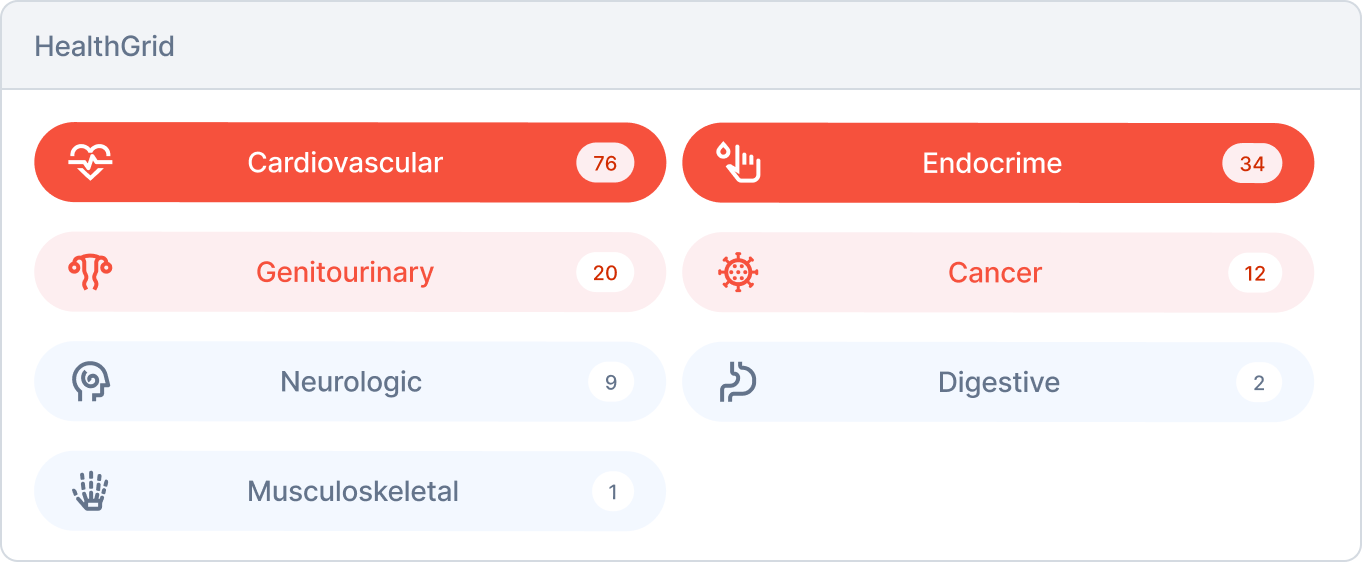

We designed a specialized component that integrates medical diagnoses, imaging exams, lab results, treatments, and medications into a visual representation of the applicant's health risks.

Clicking on any category opens a detailed view where all related medical information is displayed side by side.

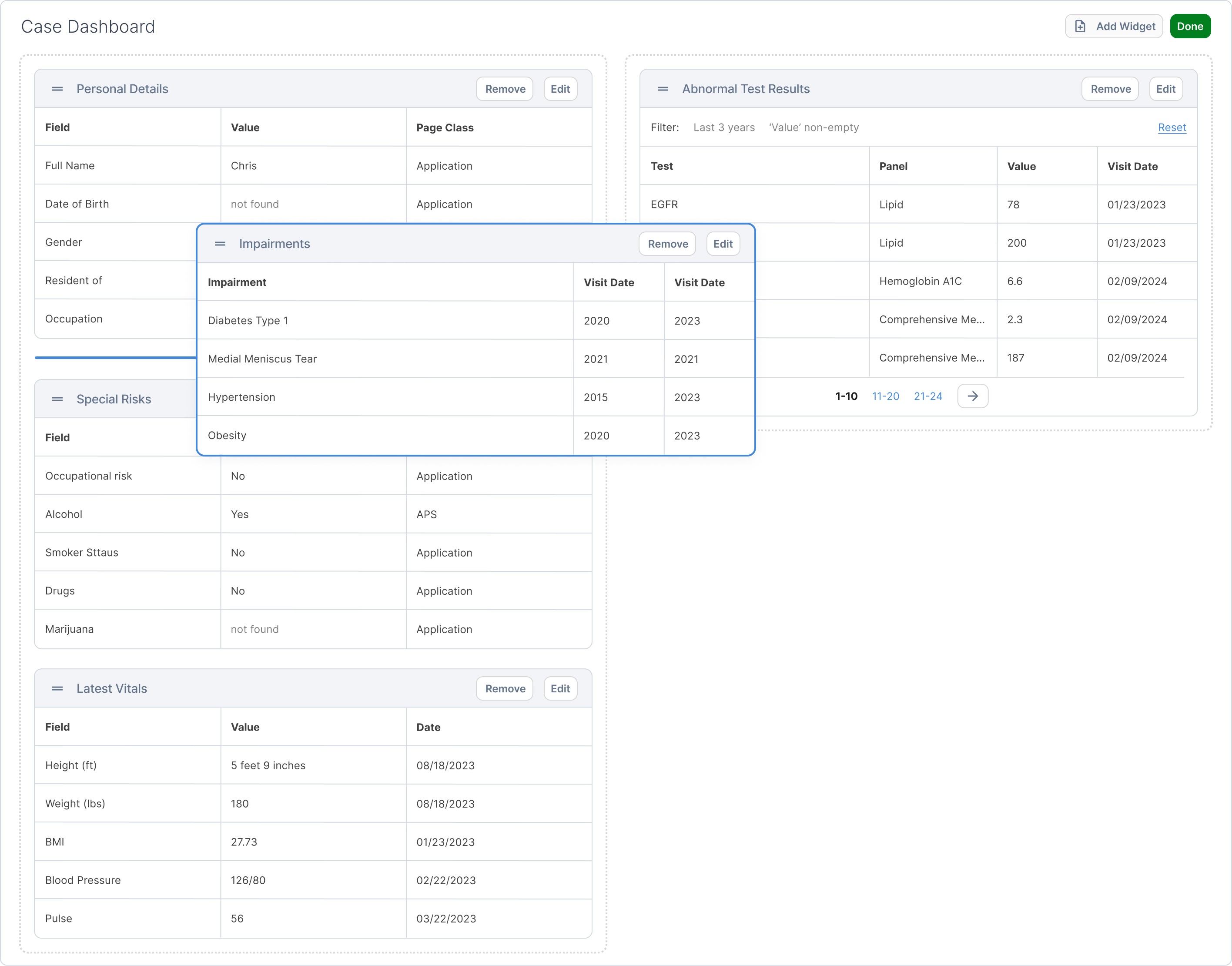

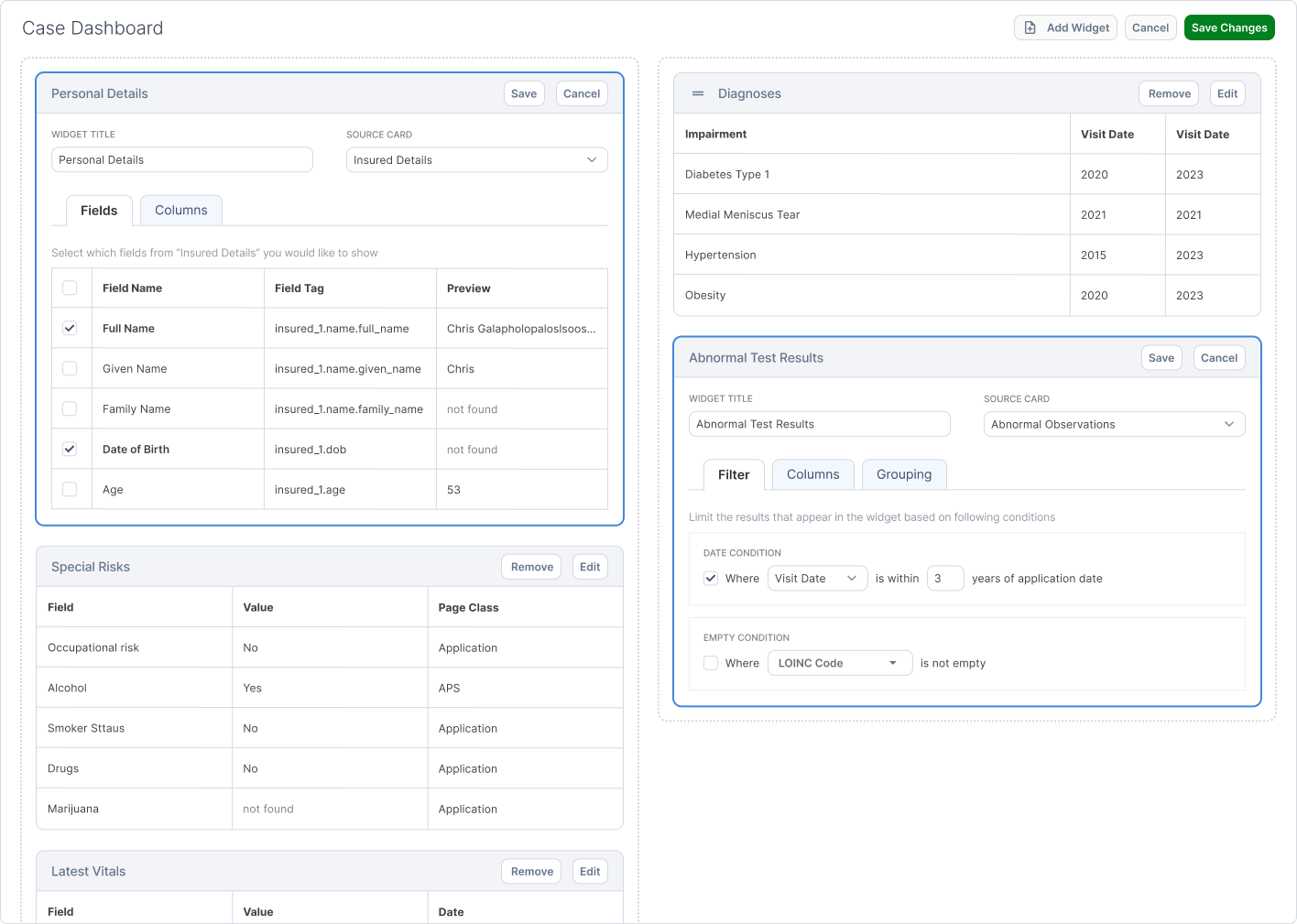

Every organization, team, and individual underwriter has unique needs and workflows. It makes no sense for the platform to impose its own order. We designed the Friendly Case Dashboard to be fully customizable. Team leads or individuals can choose what case data appears where and arrange the dashboard to their preference.

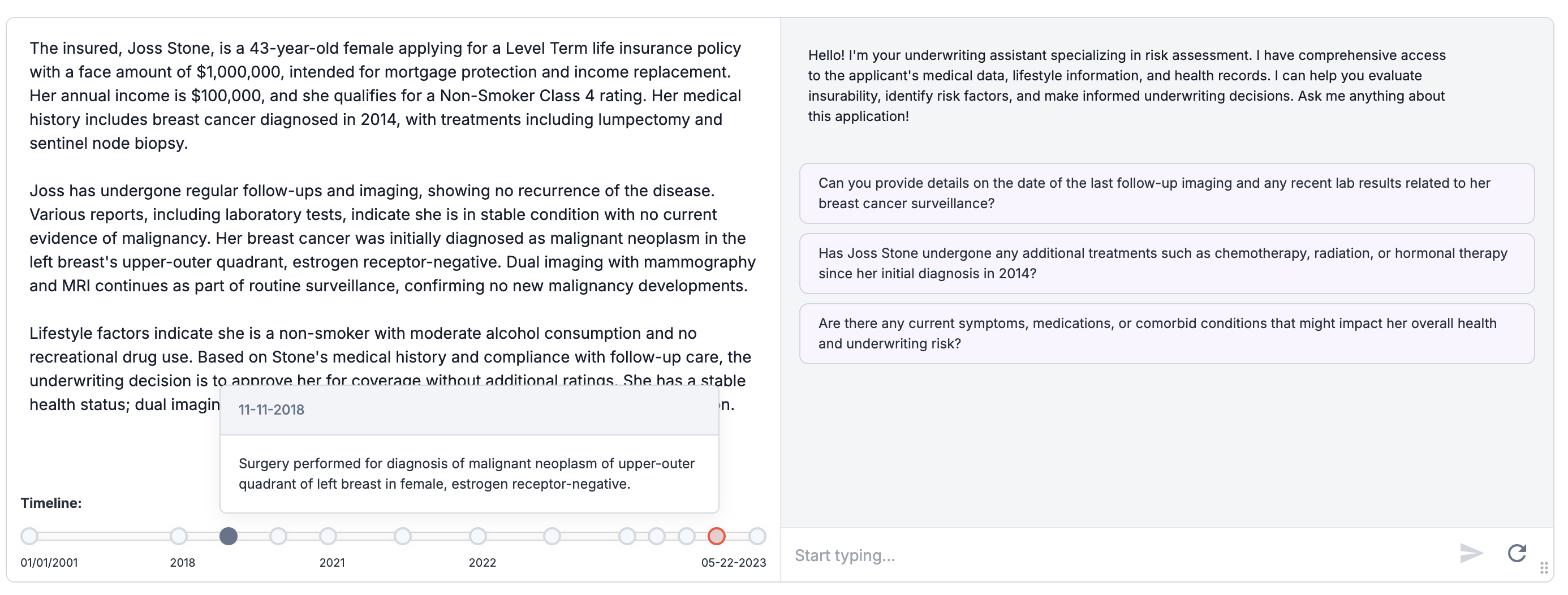

Well-organized tables of case data are beneficial, but they don’t create a cohesive story. That's why we developed a Narrative Widget that integrates the entire case into a readable narrative, an interactive timeline, and a chat feature where users can ask specific questions about the case.

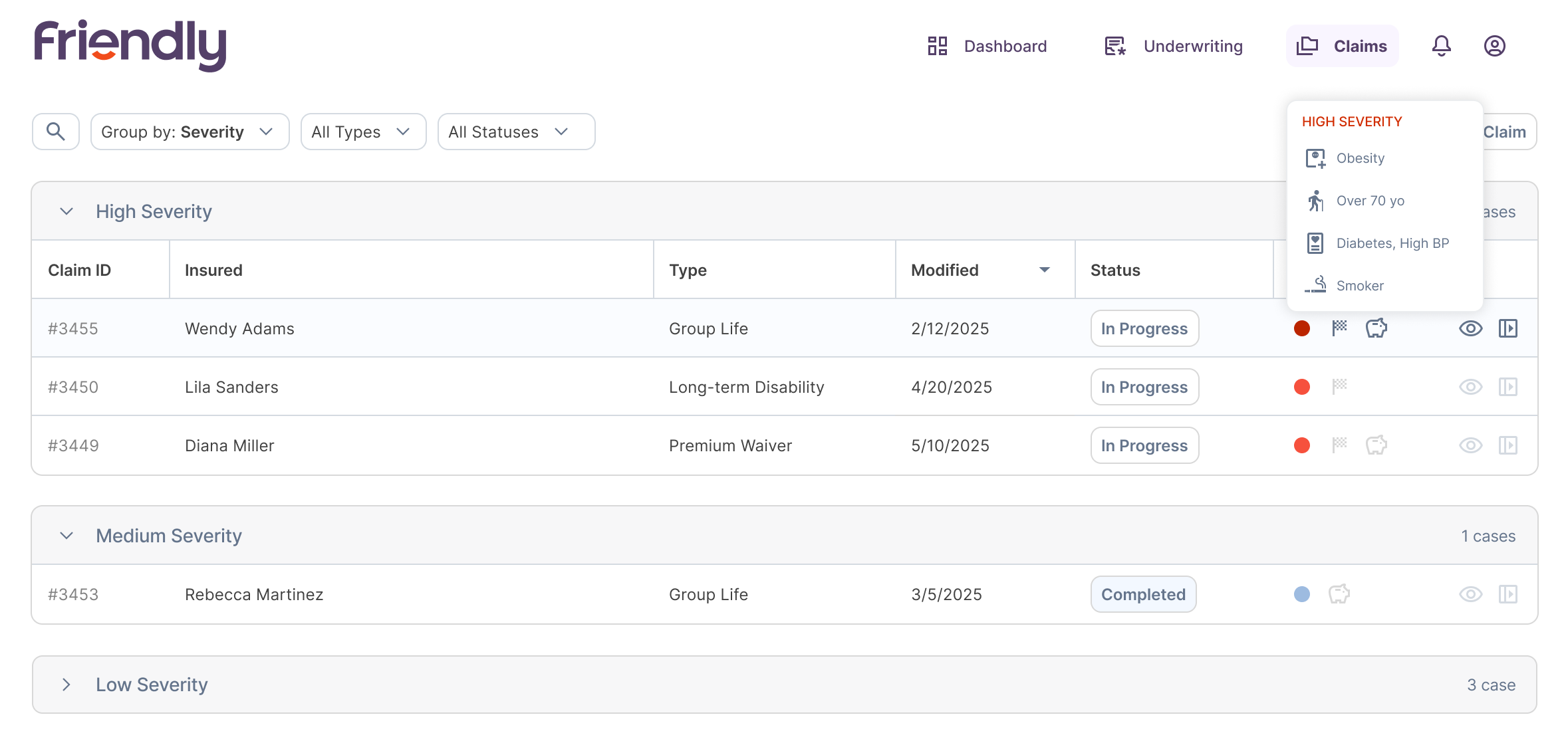

Major insurers and reinsurers often receive hundreds of applications and claims each day, and much time is wasted reading through cases that are obvious accepts or declines. Friendly addresses this by flagging and grouping cases by severity, identifying potential fraud or discrepancies, and analyzing financial data to ensure the face value is accurate.

Friendly reduced time to underwrite by 87%. What previously required reading hundreds of pages over 30-60 minutes became a one-page review in 5-10 minutes. Each underwriter could now handle 4-5x their previous caseload without additional headcount.

Beyond speed, the platform shifted how underwriters spent their time: from data extraction to judgment calls. Cases flagged as low-risk moved through in minutes, freeing experienced underwriters to focus on complex, high-value decisions where their expertise matters most.